Stock markets today provided big rises after Mario Draghi announced that he plans to buy up the debt of his favourite PIGS. The German DAX rose 2.9%, France’s CAC 40 rose 3.1%, the UK’s FTSE 100 was up 2.1% and the Spanish IBEX was up a large 4.9%. Positive market responses were not limited to Europe with the US S&P 500 also up 1.9% as I write this post.

Given these market moves let’s look at the Retirement Investing Today monthly update for the S&P500 Cyclically Adjusted PE (S&P 500 CAPE). Last month’s update can be found here.

Before we look at the CAPE let us first look at other key S&P 500 metrics:

The first chart below provides a historic view of the Real (inflation adjusted) S&P 500 Price and the S&P 500 P/E. The second chart below provides a historic view of the Real (after inflation) Earnings and Real (after inflation) Dividends for the S&P 500.

As always let us now turn our attention to the metric that this post is interested in which is the Shiller PE10. This is also shown in the first chart above which dates back to 1881 and is effectively an S&P 500 cyclically adjusted PE or CAPE for short. This method is used and was made famous by Professor Robert Shiller. It is simply the ratio of Real (ie after inflation) S&P 500 Monthly Prices to 10 Year Real (ie after inflation) Average Earnings.

As always it is important to highlight that my calculation method varies from that of Professor Shiller. He only uses S&P 500 Actual Earnings data where because I use the S&P 500 PE10 to actually make investment decisions from I also include extrapolated Earnings estimates right up to the present day. This is to try and make the value as current as possible.

The key S&P 500 PE10 metrics are:

So what of my Retirement Investing Today portfolio. Regular readers will know that I use the above PE10 data to set my allocation to the International Equities portion of my portfolio. This is strategically set at 15% of total assets and is targeted to consist of 40% US Equities, 40% Europe Equities and 20% Japan Equities. I then add the S&P500 PE10 tactical spin on top of this with a target of 10.5% allocation should the PE10 climb to 26.5 (Average PE10+10) or 19.5% should the PE10 fall to 6.5 (Average PE10-10). Therefore today my tactical allocation sets itself below 15% at 12.6%.

As always do your own research.

Assumptions include:

Given these market moves let’s look at the Retirement Investing Today monthly update for the S&P500 Cyclically Adjusted PE (S&P 500 CAPE). Last month’s update can be found here.

Before we look at the CAPE let us first look at other key S&P 500 metrics:

- The S&P 500 Price is currently 1,430 which is 1.9% above last month’s Price of 1,403 and 21.8% above this time last year’s Price of 1,174.

- The S&P 500 Dividend Yield is currently 1.98%.

- The S&P As Reported Earnings (using a combination of actual and estimated earnings) are currently $88.59 for an Earnings Yield of 6.2%.

- The S&P 500 P/E Ratio is currently 16.1 which is up from last month’s 15.9.

Click to enlarge

Click to enlarge

As always let us now turn our attention to the metric that this post is interested in which is the Shiller PE10. This is also shown in the first chart above which dates back to 1881 and is effectively an S&P 500 cyclically adjusted PE or CAPE for short. This method is used and was made famous by Professor Robert Shiller. It is simply the ratio of Real (ie after inflation) S&P 500 Monthly Prices to 10 Year Real (ie after inflation) Average Earnings.

As always it is important to highlight that my calculation method varies from that of Professor Shiller. He only uses S&P 500 Actual Earnings data where because I use the S&P 500 PE10 to actually make investment decisions from I also include extrapolated Earnings estimates right up to the present day. This is to try and make the value as current as possible.

The key S&P 500 PE10 metrics are:

- The S&P 500 PE 10 is currently 21.9 which is 1.4% above last month’s 21.6.

- The correlation between the Nominal S&P500 Price and the S&P 500 PE10 from present day back to 1881 is 0.67. This correlation is one reason why I use this metric to make investment decisions from.

- The Dataset Average S&P 500 PE10 which dates back to 1881 is 16.5. Assuming this is “fair value” it indicates that the S&P500 is still some 33% overvalued.

- The Dataset Median S&P PE10 is 15.9.

- The Dataset 20th Percentile S&P 500 PE10 is 11.0.

- The Dataset 80th Percentile S&P 500 PE10 is 20.9.

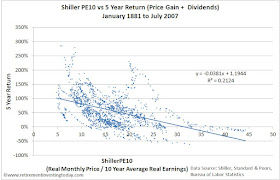

The chart below further highlights why I use the Shiller PE10 to drive a tactical portion of my Retirement Investing Today asset allocation which is stacked on top of a basic strategic asset allocation. This shows a chart of the S&P 500 vs the Nominal 5 Year Total Return from January 1881 through to July 2007. The correlation is -0.46 with an R^2 of 0.21. This implies that there is a partial correlation between the S&P 500 PE10 and future returns from the market. With the PE10 at 21.9 the trendline implies a future Nominal 5 Year Total Return of 36%. In contrast the Real (inflation adjusted) 5 Year Total Return (not shown in any chart today) trendline implies a return of 22%.

Click to enlarge

So what of my Retirement Investing Today portfolio. Regular readers will know that I use the above PE10 data to set my allocation to the International Equities portion of my portfolio. This is strategically set at 15% of total assets and is targeted to consist of 40% US Equities, 40% Europe Equities and 20% Japan Equities. I then add the S&P500 PE10 tactical spin on top of this with a target of 10.5% allocation should the PE10 climb to 26.5 (Average PE10+10) or 19.5% should the PE10 fall to 6.5 (Average PE10-10). Therefore today my tactical allocation sets itself below 15% at 12.6%.

As always do your own research.

Assumptions include:

- Prices are month averages except September ‘12 which is a 06 September ’12 S&P 500 mid market Price.

- July, August and September ‘12 Dividend is assumed to be equal to the June ’12 Dividend

- April ’12 to September ’12 reported earnings are estimates from Standard & Poor’s.

- Inflation data from the Bureau of Labor Statistics. August and September ‘12 inflation is extrapolated.

- Historic data provided from Professor Shiller website.

No comments:

Post a Comment